How Much Does It Cost To Inherit A Flat In Catalonia?

The 4 fundamental steps to calculate what you should pay when you receive an inherited flat.

Share on whatsapp

Share on linkedin

Share on twitter

Share on facebook

Tabla de contenidos

Inheriting a flat or a house in Catalonia implies a financial gain. Therefore, the heirs are forced to pay the Inheritance Tax and the tax on the Increase of Urban Nature (also known as municipal capital gains tax). In this post we will explain how the tax works and which are the most relevant reductions and bonuses that you can take advantage of in case you are about to inherit a flat in Catalonia.

What is Inheritance and Gift Tax?

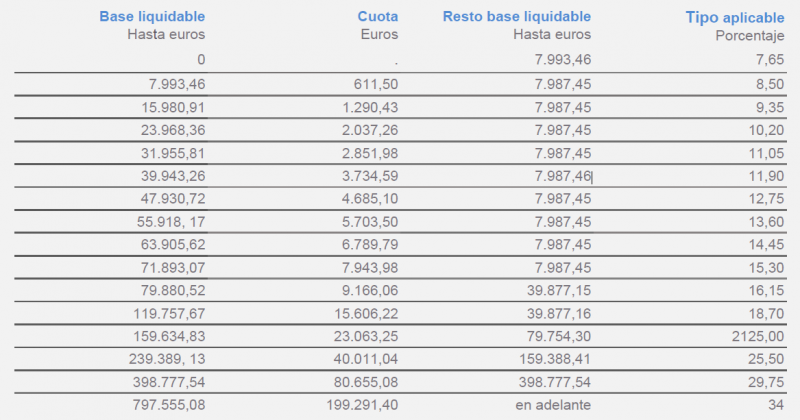

The Inheritance and Gift Tax is a tax regulated by the Spanish State and is required throughout the country. It is a progressive tax that taxes the transmission of goods and rights between natural persons. It is a tax in which there is no fixed tax percentage, but rather the more you inherit, the more you pay.

In this sense, it is possible to pay from 7.65% to 34% of what is received.

But read on and we will explain the steps to calculate it.

What is taxed? In other words, why do I have to pay a tax when I receive an inheritance or a gift?

The general principle is that the state taxes increases in the wealth of individuals. With inheritance tax, it seeks to tax the benefits obtained by you (natural person) free of charge and as a result of a death. In the case of gifts, on the other hand, the object of the tax is the increase in wealth between living persons, obtained by individuals free of charge.

How to find out how much you have to pay and how to calculate inheritance tax in Catalonia?

We would love to say that it is a simple procedure. You just fill in a form, present it to the tax office and you can go and pick up the kids from school or go out for tapas with friends. However, as with almost all tax matters, there is a high degree of complexity and technicality involved.

We will do our best to help you understand how to define what you must pay to the tax authorities when you inherit a flat in Catalonia. Technically, the amount to be paid is the tax liability.

This is calculated by multiplying the total tax liability by a multiplier coefficient established by each autonomous community.

Sounds strange and difficult to understand, doesn’t it?

Well, let’s explain it with a fairly simple analogy. Let’s imagine for a moment that we are carpenters. One ordinary day we receive an assignment: to transform a piece of wood into a fine chess piece.

Let’s try to reflect on ourselves in the workshop, scratching our foreheads and thinking through each of the steps we need to take to turn that rough piece of wood into a bishop, a rook or a pawn.

At first we will use a saw to remove the leftovers and give a more or less general shape. Then comes the chisel to define certain details, and then we move on to sanding, polishing and painting in order to finalise the figure. Something similar happens with inheritance tax.

We explain it in the following 4 steps.

The 4 fundamental steps to know how much you have to pay to the State when inheriting a flat in Catalonia

1. From the gross estate to the tax base

First it is necessary to calculate the gross estate. What in our analogy corresponds to the raw piece of wood. We need to know with a certain degree of certainty what a person’s total estate is at the time of death.

To obtain this, we must add up the actual value of the deceased’s assets plus all personal effects, household goods and furniture for his or her private use.

Then, we must obtain the net estate. To do so, we will subtract from that amount (the gross estate) the burdens, debts and deductible expenses. In the analogy, work out the shape of the wood we receive.

The next step will be to define the individual hereditary portion. Know what portion of the deceased’s estate corresponds to each heir. The net estate must be divided between each heir in accordance with the will or the legal regulations in force.

Finally, we must apply reductions to that individual inheritance portion. There are different types and each autonomous community determines its own. Below, we develop this subject in detail.

You see, our piece of wood is beginning to define its silhouette. Little by little, we begin to recognise a certain shape of a chess piece.

Now it’s time to refine it further and go into the details.

How will we do it? I recommend you to pay attention now, because here the question becomes a bit more complex.

2. Applying the tax percentage to the taxable base

Once we have the net taxable income, i.e. the net individual inheritance portion minus reductions and allowances, the next step is to apply the tax percentage to it.

How do we know which one corresponds? It varies depending on the autonomous community in which the inheritance takes place. This is because although the state regulations establish a rate of between 7.65% and 34% (Table 1), the autonomous communities are responsible for defining it.

Applying this percentage to the net tax base, we will obtain the total inheritance tax.

But the calculations do not end here.

The last step? Applying multiplier coefficients

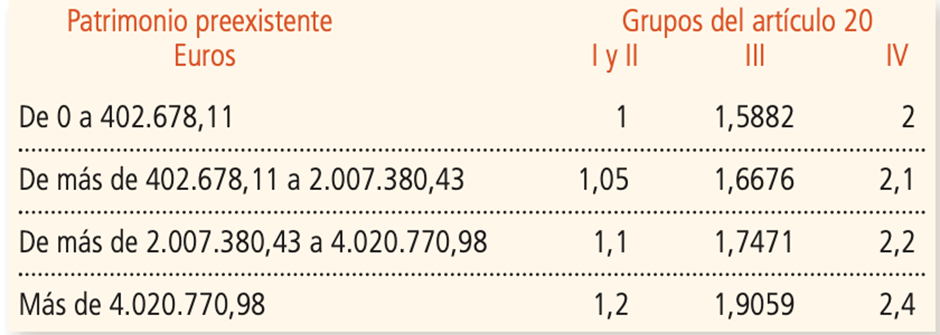

To arrive at the tax liability or what you have to pay to the tax authorities when you inherit a flat in Catalonia, you have to apply the so-called multiplying coefficients to the total inheritance tax.

How do you know which one applies to you? The coefficients vary depending on the pre-existing wealth of the heir and the relationship between the heir and the deceased.

To identify which one corresponds to your situation, the law classifies them into four groups:

Group I: descendants and adopted children under the age of 21.

Group II: descendants and adoptees aged 21 or over, spouses, ascendants and adoptive parents.

Group III: second-degree collaterals (siblings) and third-degree collaterals (nephews, uncles, aunts and uncles), and ascendants and descendants by affinity.

Group IV: fourth degree collaterals (cousins), more distant degrees and strangers.

So, to obtain the tax liability, we must multiply the total tax liability by the multiplier coefficient. This is obtained by cross-referencing the pre-existing assets of the heir with his or her degree of kinship.

We must follow the following table:

An extra benefit: reductions and bonuses – are you entitled to pay less?

Once the tax liability has been defined, deductions and allowances remain to be applied, where applicable.

In Catalonia, the Tax Agency has established a table of reductions that you can consult here.

The main ones are:

• Reductions for kinship: up to 196,000 euros.

• Reductions for disability: between 275,000 and 650,000 euros.

• Reduction for the purchase of a primary residence: 95% of the value of the home with a joint limit of 500,000 euros.

• Reduction for people over 75 years of age: from 275,000 euros.

Finally, we have finished.

The chess piece is now polished and ready to be presented. After a lot of calculations, at this point you will have a clear picture of what you will have to pay if you inherited a flat in Catalonia.

Our conclusion on Inheritance Tax.

Inheriting a flat in Catalonia involves a difficult process of rigorous steps to define the taxes to be paid. Those inexperienced in inheritance management can be overwhelmed with so much information. We recommend you follow the advice in the Practical Guide to Inheritance and Donations, prepared by the Generalitat de Catalunya.

You can also contact us if you have any doubts or if you need to delegate this management. We will be delighted to help you. We offer you all our knowledge and experience. And, as always, you are invited to leave us your opinion and questions in the comments section.