What does the new law say about the modification of the municipal capital gains tax?

The Government, by means of Royal Decree-Law 26/2021 of 8 November, has approved, with effect from 10 November 2021, the modification of the Municipal Capital Gains Tax that all owners pay when selling a property.

This new regulatory rule is based on the recent ruling of the Constitutional Court no. 182/2021 and other previous rulings already handed down by this court in 2017 and 2019 on this same issue.

The rulings of 2017 and 2019 had already set precedents…

The STC 59/2017 concluded that it was unconstitutional to demand capital gains tax in those cases in which it is subject to taxation situations that do not express economic capacity, i.e. when the land is transferred for a lower value than the acquisition value.

On the other hand, the STC 126/2019 declared that the capital gains tax is unconstitutional in those cases in which the tax to be paid is higher than the increase in capital actually obtained by the taxpayer, i.e. when the tax is paid for an amount higher than the capital gain actually produced.

The purpose of the reform is to adapt this tax to the principle of economic capacity. In other words, to comply with art. 31, 1 of the Constitution, which prevents the legislator from establishing taxes whose subject matter or taxable object does not constitute a manifestation of real or potential wealth. Therefore, it is not authorised to tax merely virtual or fictitious wealth, and, consequently, wealth that does not express economic capacity.

And this is precisely what local councils have been doing since 2004. In other words, in many cases they have been charging illegally, as the increase in the value of the land was not real but estimated.

For this reason, the TC Ruling number 59/2017 already ruled that it was not legal to tax situations of non-existent increase in the value of land.

Main changes to the tax

Now, on the basis of this TC doctrine, the Government has included a new case of not being subject to capital gains tax for cases in which it is established, at the request of the interested party, that no such increase in value has occurred.

The new regulation establishes as an objective method that the taxable base of the municipal capital gains tax will be the result of multiplying the cadastral value of the land at the time of the sale of the property by the coefficients set by each local council.

However, this objective system can alternatively be substituted so that sellers of real estate are taxed, not with the automatic application of these coefficients, but according to the increase in the real value obtained in the transaction.

As a novelty, it has now been decided that transactions in which less than one year has elapsed between the acquisition and transfer of the property will also be taxed.

In other words, the holding of the property for less than one year, which are usually those with a more speculative purpose.

This corrects a deficiency of the previous system in which this tax was not charged as it was only accrued from the year of ownership.

Two ways of determining the tax base

Objective estimation

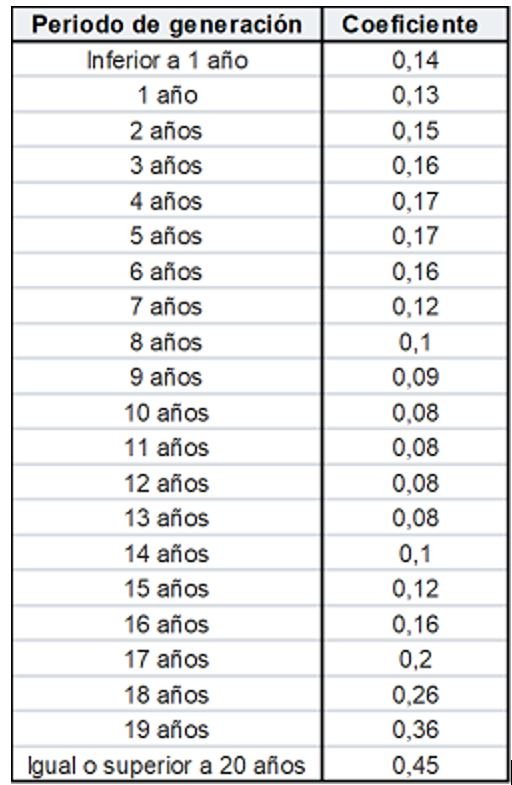

This was the system in force until now, consisting of determining the taxable base by multiplying the cadastral value of the land at the time of the sale of the property by the coefficients approved by the local council where the property is located.

These coefficients may not exceed those indicated below, depending on the number of years elapsed since the acquisition of the property:

In the case of property sales of less than one year, the full months of ownership of the property will be taken into account.

The Decree-Law now approved establishes the possibility for local councils to agree a reduction of up to 15% of the cadastral value of land, in order to adapt the amount of the tax to the reality of each municipality.

This objective system for determining the tax base becomes an optional system, which will only be applicable when the taxpayer, the seller, does not make use of the right to calculate the tax by means of:

Direct assessment

If, at the seller’s request, it is established that the increase in value resulting from the difference between the value of the land between the date of transfer and the date of acquisition is lower than that determined by the objective method, this specific increase will be taken as the tax base. This is why this system is described as direct or subjective estimation.

However, the sale and purchase values given by the seller may be subject to verification by the local councils.

The person liable for capital gains tax must declare the transfer of the property and provide the deeds documenting the transfer and previous acquisition. In this calculation procedure, expenses or taxes levied on these acquisition or transfer operations may not be deducted.

This means that the payment of the capital gains tax is no longer an automatic procedure, as it allows our tax advisor to make the calculations and tell us which calculation procedure is the most convenient for us. The City Council’s objective or the owner’s direct estimation.

Entry into force and temporary effects

The new regulation came into force on the 10th November 2021.

Local councils will have to adapt their legal framework to the provisions of the now approved royal decree-law within 6 months.

Until the municipal ordinances are adapted, the new royal decree-law will apply, using the new maximum coefficients established therein.

Possible unconstitutionality of the new reform

The TC ruling was handed down on 26 October 2021. In order to recover this important source of income for the local councils, the government has rushed to issue the Decree-Law of 10 November, through the emergency procedure.

This is precisely the reason used by some experts to consider that the urgency system used is not justified and is therefore also unconstitutional.

For this reason, they warn that the number of lawsuits to challenge it will multiply.

What happens to the unlawfully paid capital gains from the previous capital gain?

The media have been quick to say that it is not possible to claim this on the basis of what the current Constitutional Court ruling has just said.

However, this is not entirely true.

What the Constitutional Court now says in its 2021 ruling is that consolidated situations cannot be reviewed, using the current declaration of unconstitutionality and nullity for all previous cases of calculation of the tax using the objective system.

However, previous capital gains are reviewable in certain cases.

A refund of the capital gains tax can be claimed in those cases where:

There has been no expressive situation of economic capacity and,

In those cases in which the amount paid has been higher than the capital gain actually produced.

This is because in these 2 cases the review is not requested on the basis of the current ruling of October 2021, but on the basis of the aforementioned TC rulings of 2017 and 2019.

Can I appeal the tax if I have already paid it?

People who opted for a self-assessment before the TC ruling was issued can request a refund if no more than four years have elapsed.

If it was the local council that directly assessed the tax, and the officials have not yet finalised their assessment, the taxpayer has only one month to file a claim.

Many tax experts consider this tax illegal and call for its elimination. The reason is that its existence is a double taxation because taxpayers also pay the capital gain from the sale of a property in the IRPF (personal income tax).

What should I do now?

If you have more doubts and you want to know how we work, please fill in the contact form and one of our consultants will contact you to advise you.

For further information on this topic and many more you can consult other articles in our current affairs blog where you will find references on this topic and many more.

If you liked this article you can share it by clicking on the icons below, surely you have acquaintances who will like it as much as you do.